Know the Payroll Service

It can be overwhelming to do payroll for all your employees; however, you should consult with your payroll and human resources advisor for the specifics of your situation.

Finding someone who is ready to address your concerns and needs can be difficult, but H&CO's payroll experts are distinguished by a Client Services culture that keeps them fully compliant

- Hire, pay, manage, and retain employees with confidence

- Create a productive workplace: on-site, remote, hybrid

- Stay compliant with changing laws and regulations

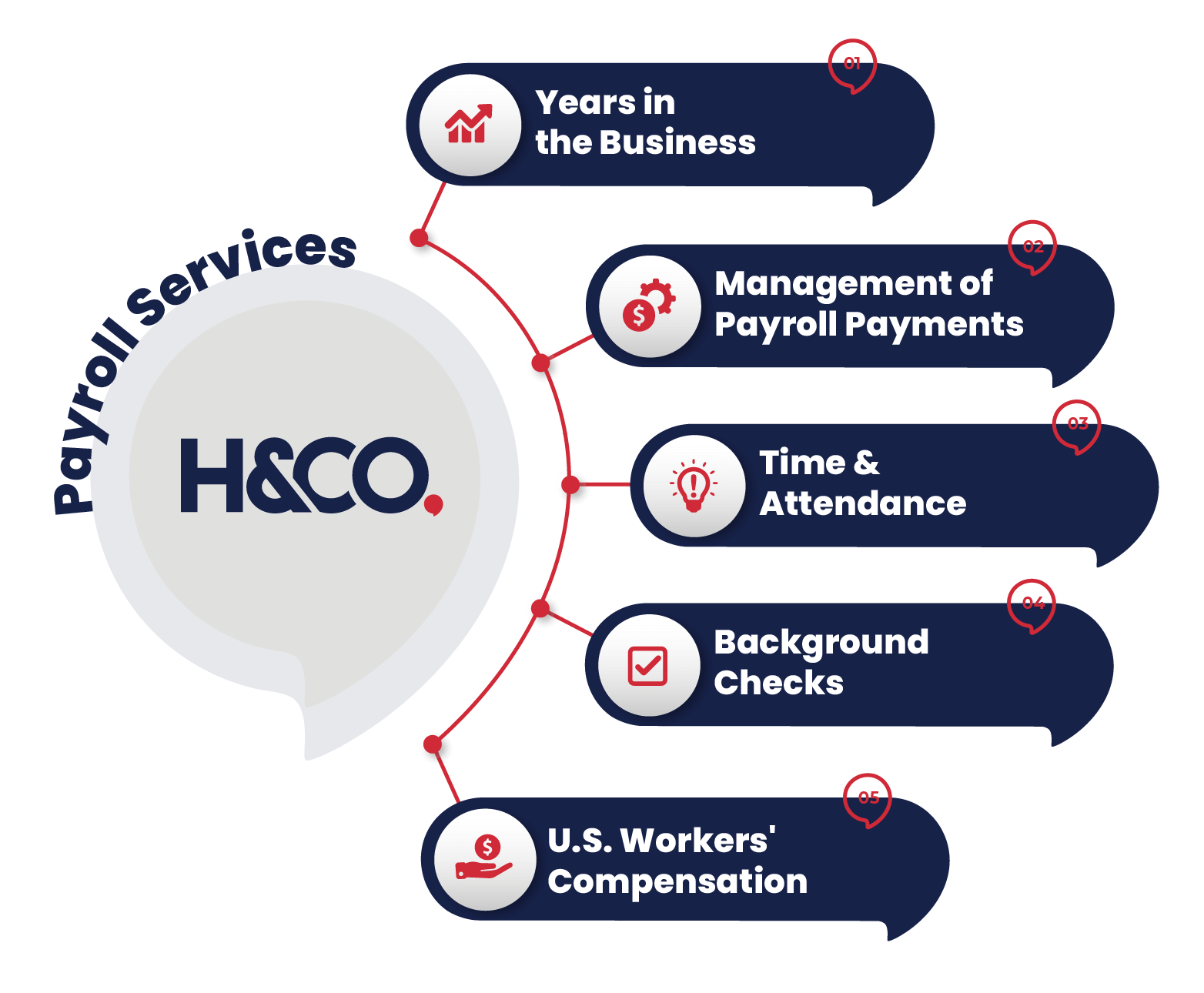

Experience You Can Count On

We are a CPA firm with a strong presence in Florida, but we also handle payroll across the country. We have over 30 years of experience that guarantee our work. Whether you prefer to prepare payroll digitally, or by email, we've got you covered!

Background Checks

Performing background checks on a potential hire candidate for your company is essential to ensuring the safety of your company and your employees.

In this way, the process is summarized in 3 easy steps: first, you must select the service package you are looking for, then you will provide us with the full name of the person to do the background search and finally, we will send you by email the results of these investigations.