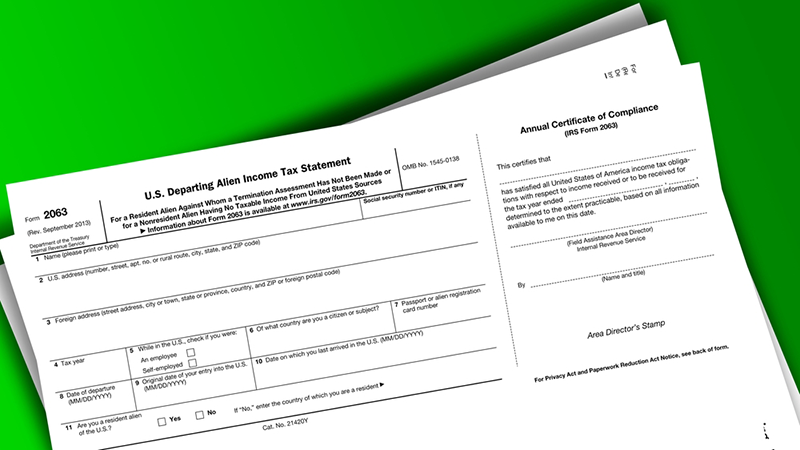

IRS Form 2063: U.S. Departing Alien Income Tax Statement

When leaving the United States, foreign nationals may face specific tax obligations depending on their residency status and income. One of the key...

When leaving the United States, foreign nationals may face specific tax obligations depending on their residency status and income. One of the key...

As the end of the year approaches, the IRS advises taxpayers to take early steps to prepare for the 2025 tax filing season. This advice is part of...

The U.S. Department of the Treasury and the Internal Revenue Service released final regulations on the foreign tax credit (FTC) on December 28, 2021....